«First

Name» «Last

Name»

«Address»

«City_», «State» «Zip»

«Date»

«Professor,

Dean, Judge or Title» «Professor, Dean, Judge or Reporter's Full Name»

«Court, Newspaper, or Law School Name»

«Address»

«City», «State» «Zip»

Dear «Professor,

Dean, Judge, or Reporter's Last Name»,

I am writing to you in order to call to your attention to, and enlist your assistance in resolving or publicizing, an apparent conflict that I have become aware of between the actual written language of the enacted statutes regarding the income tax, and the government’s claims of its applicability to the domestic income of American citizens. Under the Constitution, and according to the controlling decisions handed down by the Supreme Court in 1916, there appears to be a very real and very disturbing conflict with what was determined to be true then, and the de-facto operations that are practiced today by the IRS to allegedly effect collection of the tax.

While all Americans are encouraged to believe that the IRS’s enforcement of the income tax is lawful and necessary, I have recently come to believe that not only is that not true, but also, that it has become a very simple matter under the actual written provisions of the law to establish that claim as completely false. Thomas Jefferson spoke often of the “fruits of our labor” and the need to prevent the government from taking from the mouth of labor the fruit that it had earned, and from wasting that fruit under the pretense of taking care of the People. Today’s federal income tax collection and enforcement operations, of course, go right to the heart of the destruction of that Jeffersonian principle.

A few years ago, when I was just becoming interested in this subject, I asked the Internal Revenue Service how and why a graduated or bracketed, and therefore non-uniform, income tax was legal today, when the Supreme Court ruled in 1896 in the Pollock v. Farmer’s Loan & Trust Co. case that it was prohibited by the Constitution to enact such direct and non-apportioned, discriminatory, class legislation of that nature. I was told by the I.R.S. in response to that question, that in 1913 the 16th Amendment was adopted, authorizing the income tax as a non-apportioned direct tax, and that direct taxes do not have to be uniform.

Now, as a matter of policy, the government, through the Internal Revenue Service and its publications and website pages, routinely tells the American people that the 16th Amendment over-ruled the pre-existing provisions in Article 1 prohibiting the direct taxation of the people - unless apportioned to the states for collection and laid in proportion to the census. They claim that the 16th Amendment now authorizes the government to lay and collect taxes on income as direct non-apportioned taxes. They further state that the Supreme Court upheld the income tax as a Constitutional tax in the decision taken in the Brushaber v. Union Pacific R.R. Co. case in 1913.

However, the facts of this letter clearly demonstrate that a careful review of that Supreme Court decision (and others) reveals that the government’s claim is not true. While the Brushaber decision did indeed uphold the income tax as being a constitutional exercise by the government of the taxing powers, it did not rule that the 16th Amendment authorizes the income tax as a direct tax without apportionment. It should be immediately understood that there are enormous legal ramifications that arise as a consequence of the discovery and understanding of these historical facts.

In researching the claim that the

“We

are of opinion, however, that the

confusion is not inherent, but rather arises

from the conclusion that the 16th Amendment provides for a hitherto unknown

power of taxation; that is, a power to levy an income tax which, although

direct, should not be subject to the regulation of apportionment applicable to

all other direct taxes. And the

far-reaching effect of this erroneous assumption will be made clear …” Brushaber v. Union Pacific R.R., 240

The Court of course is, in this statement,

referring to Article 1, Section 2, Clause 3, of the Constitution, which reads:

"Representatives

and direct taxes shall be apportioned

among the several states which may be included in this union, according to

their respective numbers..."

In assessing the argument of whether or

not the 16th Amendment overcomes the un-repealed Article I command

that direct taxes be apportioned, and authorized the income tax as a direct

non-apportioned tax without also amending the language of the Article I provision

prohibiting such, the Court appears to recognize

the potential inherent conflict that would be engineered through the

acceptance of that argument and interpretation of the 16th Amendment’s

effect.

From a true reading of the decision, the Court seems to completely deny the proposition that the 16th Amendment authorizes a direct non-apportioned income tax:

“…it clearly

results that the proposition and the contentions under it, if acceded

to, would cause one provision of the Constitution to destroy another; that

is, they would result in bringing the provisions of the Amendment exempting a

direct tax from apportionment into irreconcilable conflict with the

general requirement that all direct taxes be apportioned. Brushaber v. Union

The Court clearly states that if the argument that the 16th Amendment authorizes a direct non-apportioned tax on income is accepted, without change to the Article I language prohibiting such, it

“…would cause one provision of the

Constitution to destroy another…”,

by bringing one provision of the Constitution “into irreconcilable conflict” with another. Which of course, they found untenable.

However, the Supreme Court did rule that

the income tax legislation that was tested by the Court in 1916 was constitutional. This is absolutely clear from the decision

of the Court taken in the very next case handed down in 1916, also addressing

the same income tax legislation that was tested in the Brushaber case:

"...by

the previous ruling, it was settled that the provisions of the 16th Amendment

conferred no new power of taxation but

simply prohibited the

previous complete and plenary power of income taxation possessed by Congress from the beginning from

being taken out of the category of indirect taxation to which it inherently belonged.."

It certainly would appear that the Court felt it was necessary to establish by decision that the 16th Amendment did not authorize the income tax as a direct tax without apportionment, but upheld the tax as a constitutional exercise of the indirect taxing powers. However, all of the indirect taxing powers of the federal government are possessed under Article 1, Section 8, Clause 1 of the Constitution, which of course states:

"The

Congress shall have power to lay and collect taxes, duties, imposts, and excises, … but all duties, imposts and excises shall be

uniform throughout the

Why would the Supreme Court state in the Brushaber case that the “power of income taxation” was a power “possessed by Congress from the beginning”, when the Court ruled in 1896, in the Pollock v. Farmer’s Loan & Trust Co. case, that the taxation of income by the government was not constitutional? Isn’t there a contradiction here? I mean, if it was a power possessed by Congress “from the beginning”, how on earth was it deemed not constitutional just 20 years earlier in 1896 in the Pollock case?

I believe that if we examine the different specific pieces of legislation

that were being tested in each of the two cases by the Court we find the answer

to that question. The Opinion of the Court

in the Brushaber decision clearly

states in the very first sentence of the

Opinion:

“As a stockholder

of the Union Pacific Railroad Company, the appellant filed his bill to enjoin

the corporation from complying with the income

tax provisions of the tariff act

of

Isn’t a tariff one form of an impost, which is one of the forms of indirect taxes authorized under Article I, Section 8, Clause 1? Why does it say that the Appellant (Frank Brushaber) filed this suit “As a stockholder of the Union Pacific Railroad Company”, and not as a taxpayer? Was Frank Brushaber the taxpayer in this case?

I think almost everyone supposedly familiar with this case believes that Frank Brushaber was the taxpayer who had been taxed, and who was objecting through this lawsuit to the constitutionality of the tax he had to pay. And then, the Supreme Court says the tax is constitutional, and that’s that. At least that appears to be what the government wants us to believe. Except that’s not what happened.

Why would the appellant, Frank Brushaber, attempt “to enjoin the corporation from complying with the income tax provisions of the tariff act” in his lawsuit, if he wasn’t even the taxpayer ? Wasn’t he objecting in this law suit, among other things, to the constitutionality of the tax ?

I believe that it is quite clear that Frank Brushaber actually filed this suit, not as the offended taxpayer, but as an “owner” of the company with legal standing as a stockholder, just as it says in the Opinion, in order to contest the legal burdens passed to the company by the tariff legislation being challenged in the case, in the form of an economic burden to collect tax from certain persons, to be paid over to the U.S. Treasury, and an administrative burden assumed in taking on the duty of having to properly determine from whom to collect income tax and how much to collect by withholding money as tax from payments made to subject persons. He filed the suit “as a stockholder of the Union Pacific Railroad Company”, in order to try and prevent the company from having to assume the administrative duties and economic burdens created by the company being forced by the legislation to assume the duty to act as a tax collector for the United States government.

The Brushaber

Opinion, in discussing the various contentions put forward in the case, states:

“2. The act provides for collecting the tax at the source; that is, makes it the duty of corporations, etc., to retain and pay the sum of the tax on interest due on bonds and mortgages unless the owner … gives a notice that he claims an exemption” (emphasis added)

Brushaber v. Union Pacific R.R. Co,

240

It would appear that true scheme of the income tax act implemented by the legislation being tested in 1916 in the Brushaber case, is not a scheme of direct taxation, but is clearly identified here by the Court as a scheme of indirect taxation effected by “collecting the tax at the source”. The Court appears to identify that the law establishes a legislatively created “duty” for the corporations, etc. to behave as a tax collectors and “retain and pay the sum of the tax” to the Treasury.

This legislatively created “duty”

to “retain

and pay the sum of the tax”, implementing the scheme of collecting the tax at the source, is

called withholding. It is compliance with this imposed duty,

laid on the corporation in being made a

tax collector (in the form of a Withholding

Agent), that Frank Brushaber appears to have filed the suit to enjoin.

The

legal duty, created in 1913 under the provisions of the tariff act, to act

as a tax collector and withhold money

from certain persons, i.e.: to collect tax

as a Withholding Agent, “at

the source” from non-exempt persons before those persons ever receive

payment of the funds, is still clearly contained in the provisions of the statutes

today, just as it was initially defined in the original “income tax provisions of the tariff act of October 3rd, 1913”

tested and upheld by the Court.

This legislatively created duty is defined

in the law and has been since the inception of this tax under the tariff act in

1913. Title 26 U.S.C. Section 7701 is

the code section where the controlling definitions of many terms for use within

Title 26 are contained. The term “person” is defined here, as is the term

“Withholding Agent”. The code section states in pertinent parts;:

§ 7701 Definitions.

(a) When used in this Title ...

(1). Person. – The term “person” shall be construed to mean and include an

individual, a trust, estate,

partnership, association, company or corporation.

…

(16). Withholding

Agent. - The term

"Withholding Agent" means any person

required to deduct and withhold any tax under the provisions of sections 1441, 1442, 1443, or 1461.”

A “person”,

required to withhold tax as a “Withholding

Agent”, is not just an individual, but may also be a company or a “corporation,

etc”, precisely as identified by the Supreme Court in the Brushaber decision.

Section 7701(a)(16), defining the Subtitle A income tax Withholding Agent, establishes the complete and entire authority contained in the statutes to “retain and pay the sum of the tax”, as identified by the Supreme Court in the Brushaber decision. It is the Withholding Agent who must act as a tax collector and “retain and pay the sum of the tax” by withholding income tax from subject persons as directed by the language of the Subtitle A statutes of Title 26.

From a simple reading of the statutes we

see that it is this legislatively defined “Withholding

Agent” who is tasked by the statutes with the duty to withhold the income

tax at the source, i.e.: from payments made,

and then, acting as a tax collector, pay over those withheld funds to the U.S.

Treasury as tax. The

Withholding Agent is the only “person” authorized under Subtitle A to collect tax at the source, by withholding money as tax

from payments made to subject persons.

The legal definition of the term “Withholding Agent” is simple and

straight-forward. To understand its

complete enacted legal authority all one need do is read the actual code

sections invoked by the statutory definition shown above in Section 7701(a)(16).

The only code sections cited in the

statutory definition of the Withholding

Agent at 26 U.S.C. § 7701(a)(16) are Sections 1441, 1442, 1443, and 1461. Section

1441 provides:

§

1441. Withholding of Tax on Nonresident Aliens

(a) General rule. Except as otherwise provided in subsection (c)

all persons, in whatever capacity acting

having the control, receipt, custody,

disposal or payment of any of the items

of income specified in subsection (b) (to the extent that any of such items

constitutes gross income from sources within the United States), of any nonresident alien individual,

or of any foreign partnership shall deduct and withhold from such items a

tax equal to 30 percent thereof, except that in the case of any items of income specified

in the second sentence of subsection (b), the tax shall be equal to 14 percent

of such item. (emphasis added)

(b)

Income items. The items of income referred to in subsection (a) are interest (other

than original issue discount as defined in section 1273), dividends, rent,

salaries, wages, premiums, annuities, compensations, remunerations, emoluments,

or other fixed or determinable annual or periodical gains, profits, and

income,...

Clearly, Section 1441 only authorizes and requires the Withholding Agent to withhold income tax from non-resident alien “persons”, while subsection (b) clearly states that it is not just the interest due on bonds and mortgages that is subject to the withholding of income tax, as was the specific subject circumstance in the Brushaber case, but that all of the different forms of earnings listed, of these non-resident alien persons, are subject to the withholding of the income tax as well, listing dividends, rent, salaries, wages, premiums, annuities, etc.

Section 1442, the next code section referenced in the definition of the Withholding Agent provides that foreign corporate “persons” (companies) shall be treated similarly:

§ 1442 Withholding of Tax on Foreign Corporations

(a)

General

rule.

In the case of foreign corporations subject to taxation under this subtitle,

there shall be deducted and withheld at

the source in the same manner and on the same items of income as is provided in Section 1441 a tax equal to 30%

thereof. ....

It is not

necessary to examine the specific language of Section 1443, the next

code section referenced in the definition of the Withholding Agent, it simply provides for slightly modified withholding

treatment for certain foreign tax exempt organizations. It is titled:

§

1443 Foreign Tax Exempt

Organizations

These code sections, specifically invoked

by actual written reference in the statutory definition of the “Withholding Agent”, only authorize the withholding of Subtitle A

income tax from foreign “persons”.

Is that because these income tax

provisions are the original income tax provisions of the tariff act of October

3rd, 1913, still preserved in the law, in order to be used to

demonstrate the actual true force of the written law? Does a tariff only apply to foreign goods and foreign economic activity, thus, could only be withheld from foreign

persons as directed in the

identified statutes? Is there some other statute implementing the

identified scheme of the income tax legislation of “collecting the tax at the source”, authorizing the tax to be

collected from any other person other than the foreign persons identified in statute by

Section 1441 and 1442? Is that why there

is no code section that exists in Subtitle A that authorizes the withholding of

income tax from any other persons, including American citizens? Or even resident

aliens, as opposed to non-resident aliens under Section 1441?

It would appear, just as it was identified

by the Supreme Court in the controlling decisions of Brushaber and Stanton in

1916 settling the matter of the constitutionality of the income tax laws, that this

is how the income tax is legitimately

imposed, collected, and enforced. INDIRECTLY,

by third party Withholding Agents, acting

as tax collectors for the U.S. Treasury who shift the burden of the tax from themselves as tax collectors by withholding the tax from the foreign “persons” who

are the true subjects of the tax and the

intended taxpayers, and who are actually

made subject to the withholding of tax from their payments by the provisions of the statutes.

“Ordinarily, all taxes paid primarily by persons who can shift the burden upon someone else … are considered indirect taxes;”

Pollock v. Farmer’s Loan & Trust Co.,

157

Is this why the Supreme Court said this

legislation was inherently indirect? Did

Congress, in authoring this legislation for an indirect tax specifically take

its “cues” on how to properly do so from the Pollock ruling, and design a tax that is collected indirectly by

tax collectors in the form of Withholding

Agents, who shift the burden of the

tax from themselves as payors (collectors), onto the intended subject foreign

taxpayers by withholding? Or, is it

because a tariff is actually one form of an impost, which is one of the three

types of indirect taxes authorized

under Article I, Section 8, Clause 1 for Congress to lay and collect?

Section 1461 is the last code section referenced in the statutory definition of the Withholding Agent provided by 26 U.S.C. § 7701(a)(16). It explicitly states

§

1461 Liability for withheld

tax.

Every person required to deduct and

withhold any tax under this chapter

is hereby made liable

for such tax and is hereby

indemnified against the claims and demands of any person for the amount of any

payments made in accordance with the provisions of this chapter.

This section clearly says that it is the Withholding Agents who are made liable for the payment of the income taxes

that they have collected from other

persons, while acting as tax collectors, by withholding money as tax from payments

made to “persons” who are made

subject by the provisions of the statutes to the withholding of tax from their

payments. Those persons, under the statutes, are all foreign. The statutes do not make the Withholding Agent, or any other “person”, for that matter, liable for the payment of income tax on his own income because that would be

unconstitutionally direct taxation. The Supreme Court upheld this income tax

legislation specifically because it only enacted the limited, indirect tax

found in the statutes, that is

collected at the source by third party tax collectors in the form of “Withholding Agents”, who shift the burden of the tax they are

liable for by withholding money as tax from subject persons, who, as

expected under the provisions of a tariff act, are all foreign.

It would appear that while Section 1 indeed imposes a tax on individuals, it does not state how the tax is to be collected, or where, or from whom it is to be collected, and how. And it certainly does not state who is actually liable to pay the tax as neither the word “liable” nor “liability“ occur anywhere within its contents. The Supreme Court identifies in the Brushaber decision that it is the Withholding Agent under the scheme of collecting the tax at the source who is made responsible for the collection of the Subtitle A income tax. Section 1461 clearly says that those Withholding Agents are the persons made liable for the payment of the income tax that they have collected from those other persons, the subject taxpayers. The only persons made subject to the withholding of income tax that can be identified in the Subtitle A statutes are all foreign “persons” under Sections 1441, 1442 and 1443.

The only way to arrive at the conclusion that under the provisions of Subtitle A American citizens owe an income tax on the fruits of their own domestic labor or income, is to assume that Section 1, in addition to imposing the tax on individuals, also makes those same individuals liable directly for the tax without the statute actually saying so. As stated, Section 1 does not actually contain the words liable or liability, or make any specification of such liability for tax in any other manner, and of course, allowing that assumption to be made is improper.

Since the argument that the 16th Amendment authorized the income tax as a direct non-apportioned tax was clearly rejected by the Supreme Court through the Brushaber and Stanton rulings in 1916, and since there are no intervening judicial authorities in the interim, and since the legislation has never again been reviewed and tested by the Supreme Court, can you explain to me how the income tax is legitimately imposed and collected from citizens today by the I.R.S. as though it were a direct tax? What is the legitimate, lawful basis for the direct implementation and enforcement operations undertaken against individual citizens today by the IRS in the name of income tax?

Under the actual provisions of code sections 1441, 1442, and 1443, the only “persons” subject to the withholding of income tax under Subtitle A are all foreign. Where is the statute in Subtitle A implementing the avowed scheme of collecting the tax at the source and granting the authority to collect an income tax by withholding from payments, or in any other manner, from American citizens? Or even from resident aliens as opposed to non-resident aliens as identified in Section 1441? Those statutes, relating to citizens and the provisions for the withholding of income tax from them, do not appear to actually exist anywhere in Subtitle A.

Is that because that power would be unconstitutionally direct, and because the income tax is actually a tariff which is laid only on foreign activity, not the domestic activity of the American People?

Under the Constitution the federal

government is of course allowed to tax foreign activity in the United States,

but still, even after the passage of the 16th Amendment according to

the Supreme Court, may not tax

citizens, their property, their earnings, or

the fruits of their labor in the form of income, directly, because that

would bring multiple provisions of the Constitution “into irreconcilable conflict” with one another and “would cause one provision of the

Constitution to destroy another”.

Another case, Eisner v. Macomber, handed down in 1920 shortly after the Brushaber and Stanton decisions, appears to again confirm the Courts masterful understanding of all of the circumstances in play:

“Thus, from

every point of view we are brought irresistibly to the conclusion that neither under the Sixteenth Amendment nor

otherwise has Congress power to tax without apportionment a true stock

dividend made lawfully and in good

faith, or the accumulated profits behind

it, as income of the stockholder.” Eisner

v. Macomber, 252

While this decision appears to be more

about the technical definition of the term “income” to be relied upon by the

Treasury, requiring a “gain” that must actually be realized by actual payment

to the shareholder before it can become identifiable as taxable income to that

shareholder, please note that the Court didn’t simply say that. They took the time to state “…that neither

under the Sixteenth Amendment nor otherwise has Congress power to tax without

apportionment…”.

They further state:

“The Revenue Act of 1916, in so far as it imposes a tax upon the stockholder because of such

dividend, contravenes the provisions of article 1, 2, cl. 3, and article 1, 9,

cl. 4, of the Constitution, and to this extent is invalid, notwithstanding

the Sixteenth Amendment.” Eisner

v. Macomber, 252

Seven years after the adoption of the 16th

Amendment, the Supreme Court again says, based on the Pollock decision in 1896, that it

is still unconstitutional to tax income directly, despite the 16th Amendment’s ratification.

This decision, Eisner v. Macomber, was handed down in

1920, 4 years after the Brushaber decision in 1916. While many do not understand this ruling

because it seems to contradict the two previous Supreme Court rulings, Brushaber

& Stanton,

upholding an income tax, upon closer examination we find that the rulings are not contradictory at all, but

are all consistent. Capably differentiating in the various pieces of

legislation being tested in the different cases, the difference between legitimate and constitutional indirect taxation

by the laying of a tariff that is collected indirectly at the source by tax

collectors withholding tax from payments made to foreign persons subject to the

provisions of a tariff act, and the unconstitutionally

direct taxation that would be constituted by the direct taking of a citizen’s income

in the form of dividends, and otherwise without basis as an indirect tax

under Article I, Section 8, Clause 1.

Eisner,

quite simply, marks the

Court’s ability to distinguish between the holdings in the

previous cases of 1916 (Brushaber &

Stanton), where the income tax legislation of the tariff act that was

being tested in that case was found to be constitutional as an indirect tax, and the Eisner

and Pollock decisions which

declared the taxation of income without

apportionment attempted by the

legislation tested in those cases, to be

totally unconstitutional and unsustainable.

That Pollock decision

speaks quite clearly and forcefully as to the court’s true feelings in 1896 about

a direct income tax:

"... a tax upon property holders in respect of their estates,

whether real or personal, or of the

income yielded by such estates, and the payment of which cannot be avoided, are

direct taxes..." Pollock v. Farmer’s Loan & Trust Co., 157

and;

“… it is apparent (1) that the

distinction between direct and indirect taxation was well understood by the

framers of the constitution and those who adopted it; (2) that, under the state

system of taxation, all taxes on real estate or

personal property or the rents or income thereof were regarded as direct taxes;”

Pollock v. Farmer’s Loan

& Trust Co., 157 U.S.

429, 574 (1895)

and;

“The income tax law under

consideration is marked by

discriminating features which affect the whole law. It discriminates

between those who receive an income of $4,000 and those who do not. It thus vitiates, in my judgment, by

this arbitrary discrimination, the whole

legislation. Pollock v. Farmer’s Loan & Trust Co.,

157

and;

“We are of

opinion that the law in question, so far

as it levies a tax on the rents or income of real estate, is in violation of the constitution, and is

invalid.” Pollock v. Farmer’s Loan

& Trust Co.,

157

The

"...Ordinarily, all taxes paid primarily by persons who can shift the burden upon someone else, … are considered indirect taxes; but a tax upon property holders in respect of their estates, whether real or personal, or of the income yielded by such estates, and the payment of which cannot be avoided, are direct taxes..."

and, from Justice Fields’ supporting opinion in the matter;

“I am of opinion that the whole law of 1894 should be declared void, and without any binding force,-that part which relates to the tax on the rents, profits, or income from real estate, that is, so much as constitutes part of the direct tax, because not imposed by the rule of apportionment according to the representation of the states, as prescribed by the constitution; and that part which imposes a tax upon the bonds and securities of the several states, and upon the bonds and securities of their municipal bodies, and upon on the salaries of judges of the courts of the United States, as being beyond the power of congress; and that part which lays duties, imposts, and excises, as void in not providing for the uniformity required by the constitution in such cases” Pollock v. Farmer’s Loan & Trust Co., 157 U.S. 429, 608 (1895)

and;

“The inherent and fundamental

nature and character of a tax is that of a contribution to the support of the

government, levied upon the principle of

equal and uniform apportionment among the persons taxed, and any other exaction does not come within the

legal definition of a 'tax.'” Pollock

v. Farmer’s Loan & Trust Co.,

157

and;

“The legislation, in the discrimination it makes, is class

legislation. Whenever a distinction

is made in the burdens a law imposes or in the benefits it confers on any

citizens by reason of their birth, or wealth, or religion, it is class

legislation, and leads inevitably to oppression and abuses, and to general

unrest and disturbance in society. It was hoped and believed that the great

amendments to the constitution which followed the late Civil War had rendered such legislation impossible

for all future time. But the objectionable legislation reappears in the act

under consideration.” Pollock v. Farmer’s

Loan & Trust Co.,

157

Are “the great amendments

to the constitution which followed the late Civil War” referenced here, a

reference to the 14th Amendment containing

the equal protection clause of the Constitution? When it states that it was hoped that such

Amendment “had rendered such legislation

impossible for all future time”, is that because a graduated income tax

with different tax rates for different tax brackets based on levels of earnings

like we have in today’s law, effectively establishing different classes in our

society that are treated differently under the law, should be and would be deemed unconstitutional under that equal

protection clause? Why isn’t that

still true today, if, as the Supreme Court stated in the

And, in recognition of the long since forgotten constitutional

limitations on the federal power to tax, Justice Fields continues:

“There is no such thing in the theory of our national government as unlimited

power of taxation in congress. There are

limitations, as he justly observes, of its powers arising out of the

essential nature of all free governments; there are reservations of individual

rights, without which society could not exist, and which are respected by every

government. The right of taxation is

subject to these limitations. Citizens'

Savings Loan Ass'n v.

and;

“Although there

have been from time to time intimations that there might be some tax which was

not a direct tax nor included under the words 'duties, imposts, and excises,' such a tax for more than one hundred years

of national existence has as yet remained undiscovered, notwithstanding the

stress of particular circumstances has invited thorough investigation into

sources of revenue.” Pollock v. Farmer’s

Loan & Trust Co.,

157

And finally,

“Here I close my opinion. I

could not say less in view of questions of

such gravity that go down to the very foundation of the government. If the

provisions of the constitution can be set aside by an act of congress, where is

the course of usurpation to end? The present assault upon capital is but the

beginning. It will be but the stepping-stone to others, larger and more

sweeping, till our political contests will become a war of the poor against the

rich,-a war constantly growing in intensity and bitterness. 'If the court

sanctions the power of discriminating taxation, and nullifies the uniformity

mandate of the constitution,' as said by one who has

been all his life a student of our institutions, 'it will mark the hour when the sure decadence of our present government

will commence.' If the purely arbitrary limitation of four thousand dollars

in the present law can be sustained, none having less than that amount of

income being assessed or taxed for the support of the government, the

limitation of future congresses may be fixed at a much larger sum, at five or

ten or twenty thousand dollars, parties possessing an income of that amount

alone being bound to bear the burdens of government; or the limitation may be

designated at such an amount as a board of 'walking delegates' may deem

necessary. There is no safety in allowing the limitation to be adjusted except in strict compliance with the

mandates of the constitution, which require its taxation, if imposed by direct taxes, to be

apportioned among the states according to their representation, and, if imposed by indirect taxes, to be uniform

in operation and, so far as practicable, in proportion to their property,

equal upon all citizens. Unless the rule of the constitution governs, a

majority may fix the limitation at such rate as will not include any of their

own number.” Pollock v. Farmer’s Loan & Trust Co.,

157

According to the Supreme Court, all of these arguments identified by Justices Fuller and Fields in 1896 remain unaffected by the adoption of the 16th Amendment in 1913, as the Court said in the Stanton decision that the 16th Amendment “conferred no new power of taxation”, and that the income tax that is laid in statute by the act tested “is inherently indirect”. So none of these issues addressed in Pollock concerning the prohibition on direct taxation would appear to have ever been touched by the rulings in the Brushaber, Stanton, and Eisner cases, or by any other case concerning income tax that has ever been reviewed by the Supreme Court after the adoption of the 16th Amendment. In fact, as late as 1920, in the Eisner decision, the Court is still referring to and relying upon the Pollock ruling to settle the later disputes.

The Pollock decision has never been overturned by the Supreme Court, and is not legitimately, implicitly overruled by the adoption of the 16th Amendment. Pollock and Eisner upheld the constitutional prohibition on direct taxation without apportionment, even after the ratification of the 16th Amendment in the case of Eisner, while Brushaber and Stanton upheld the federal power to tax indirectly, by having third party Withholding Agents, acting as tax collectors, collect tax by withholding money as tax from payments made to foreign persons. This is all done under the provisions of an indirect impost in the form of a tariff act that applies to foreign goods entering the country and to foreign activity occurring within the country.

The cases address different issues and aspects of the

Constitution entirely, one addressing the violation of the limits of the power

to tax directly if done so without

apportionment, the other addressing the legitimate exercise of the power to uniformly tax indirectly. They do not contradict or conflict with one another,

but rather work hand in hand to uphold the clear distinction between, and

limits of, the two great classes of taxing powers established in the

Constitution for the federal government to exercise.

The “persons”

made subject to the withholding of income tax from their payments are all

foreign of course because these legislative provisions are the “income tax provisions of the tariff act of

Oct. 3, 1913” that the Chief Justice White refers to in the first sentence

of the Brushaber decision of the

Supreme Court, upholding the constitutionality of the tariff legislation that

was tested in that case. A tariff is an

impost, which is a foreign tax, and only foreign

persons or persons involved in foreign

activity are subject to the payment of it. The power to lay tariffs on foreign imports

and activity is a “complete and plenary”

indirect power to tax that has been

possessed by Congress from the beginning under Article 1, Section 8, Clause 1

of the Constitution, again, precisely as identified by the Supreme Court in the

There is no other code section anywhere in

Subtitle A, besides Section 1461, making any other person or party liable for

the payment of any Subtitle A income tax. In fact, the only other code section in all

of Title 26 that specifies that any other person or party is liable for the

payment of the income tax is Title 26

U.S.C. § 3403, from Subtitle C of

Title 26, which states;

§

3403. Liability for tax

The employer

shall be liable for the payment of

the tax required to be deducted and withheld under this chapter, and shall not be liable to any person

for the amount of any such payment.

Again, we find that the statutes are

consistent. In the Subtitle C provisions

adopted in 1944, just like in the Subtitle A provisions adopted in 1913 and

tested by the Supreme Court in 1916, we find again that it is the tax

collector who is made liable in

the statutes for the payment of the income tax. In Subtitle A, the Withholding Agent is made liable for the payment of the income tax

that he has withheld from foreign “persons”,

and in Subtitle C it is the “employer”,

another “person” acting in the

capacity of a tax collector,

that is made liable for the payment of

the income tax that he has also withheld

from other persons, his

participating employees in this case.

Sections 1461 and 3403 are the only statutes in all of Title 26 that

make any persons liable for payment of the income tax. By making only the tax collectors,

acting in the capacity of a either a “Withholding

Agent” or an “employer”, liable by statute for the

payment of the withheld income taxes,

the statutory scheme for the collection and enforcement of the income tax as

enacted in 1913 is kept entirely indirect, and therefore, as found by

the Supreme Court, is constitutional as

an indirect tax laid on foreign activity in the United States.

It

is not constitutional because the Constitution now allows direct non-apportioned

taxation of the people under the 16th Amendment, as the government claims

and wants the People to erroneously believe, but because the Subtitle A statutes

only actually implement a very indirect income tax that is collected

and paid by third-party tax collectors (Withholding

Agents) who shift the burden of the tax they pay by withholding the tax

from other persons who are the actual

taxpayers, and who are made subject by

law to the withholding of money as tax from their payments, and who, under

the law are all foreign “persons” properly subjected to the

provisions of a tariff act.

The Title 26 statutes of Subtitle A do not

make the sovereign American people themselves the direct subject taxpayers of

the income tax. Nor do the statutes of

Subtitle C. The legislation actually

enacted, correctly recognizes the true and proper role of the Sovereign in any

system of taxation, and makes the American people the tax collectors, as sovereign citizens are the “etc.” referenced in the

duty of the “corporations, etc.” referred to in the Brushaber decision cited above. I repeat, it appears that it is absolutely

clear that the true legal role of the

American people in the income tax collection system actually enacted under

the written provisions of the statutes, is

the role of the tax collector, acting as a “Withholding Agent”, and that We

the People, while we are made the payors

of the tax as collectors of it, we are not the identified proper subjects

of the income tax, nor are we assigned the role of the taxpayer by the

provisions of the statutes. That

role is reserved for the foreign subjects of the federal government.

By injecting this third party, the Withholding Agent, into the scheme for “collecting the tax at the source”, the burden to pay the income tax is shifted by

withholding from the payor of the tax - the tax collector, the Withholding Agent, to the actual taxed subject and real taxpayers

- the non-resident aliens and foreign

corporations that are the proper taxed subjects of the federal government

under the Subtitle A provisions of the tariff act, and, under the Constitution.

“Ordinarily, all taxes paid primarily by

persons who can shift the burden upon someone else, or who are under no legal

compulsion to pay them, are considered indirect taxes;” Pollock v. Farmer’s Loan & Trust Co.,

157 U.S. 429, 558 (1895)

The injection of this third party, the Withholding Agent, into the Subtitle A

income tax collection scheme of “collecting

the tax at the source”, keeps the income tax indirect because the tax is collected by a third party – the Withholding Agent, and the burden is

shifted through withholding from that third party tax collector to the subject

foreign taxpayer.

Under the actual provisions of the

statutes, the tax is not collected

directly by the government from the subject taxpayer, but is collected

indirectly by the third party Withholding

Agents. Under the actual provisions of the statutes,

the sovereign American citizens are not

taxed directly and are not cast in

the role of subject taxpayers, but rather are empowered as tax collectors.

It is the subject foreign non-resident persons,

individuals and corporations, that are actually cast in the role of the subject taxpayers by the language of the statutes implementing the “income tax provisions of the tariff act of

Oct. 3, 1913”, now known as Subtitle A of Title 26.

Additionally, Section 1463 clearly states

who is to be penalized if the tax is not properly withheld and paid into the

U.S. Treasury as proscribed by these statutes;

§ 1463. Tax paid by recipient of income

If—

(1) any person, in violation of the provisions of this chapter, fails to deduct and

withhold any tax under this chapter, and

(2) thereafter the tax against which

such tax may be credited is paid,

the tax so required to be deducted and withheld shall not be

collected from such person; but this section shall in no case relieve such person from

liability for interest or any penalties or additions to the tax otherwise

applicable in respect of such failure to

deduct and withhold.

This code section says that it is the Withholding Agents who

are responsible for and must pay the

penalties, interest, and additions to

tax that are due on the income tax that was not properly withheld,

reported, and paid into the Treasury. It

is not the actual taxpayer who is penalized by any of these penalties or

additions by this statute, it is the tax collector, or Withholding

Agent, who is penalized. Again, this keeps the tax and its enforcement

under the statutes, indirect. If

the actual taxpayers were made subject to

interest, penalties and additions to tax,

that would be unconstitutionally direct taxation without apportionment and

would be a violation of the Constitution.

The analogy one can very quickly and

easily make is that of a sales tax collected by the stores in the fifty states.

The sales tax is an indirect tax that is not imposed on any person, per se, but

on certain transactions. When it is

imposed on a transaction it is collected by a third party, the tax collector, the store. It is not collected by the government itself

from the taxpayer. The government deals

only with the tax collector, the store, not

the taxpayer.

And it is the store, the tax collector, that is made liable for the payment of the tax to the Treasury, not the customers, the actual

taxpayers. Finally, if the tax collector

(the store) fails the duty to collect

the sales tax as required, it is again

the tax collector (that store), and

not the customer taxpayer, that is contacted and punished for that failure

and made liable for penalties, fines, and additions to tax thereby

incurred. The collection of the federal

income tax is obviously properly effected under the true provisions of the

Subtitle A statutes in exactly the same

indirect manner, with the “Withholding

Agent” being cast in the role of the tax collector, just as the store is

cast as the tax collector in the states’ programs for the collection of their

sales taxes.

It

is clear that under the true provisions of the statutes of Subtitle A, the

income tax is a tax that is collected indirectly at the source by

withholding. Under the provision of the

statutes, it is the tax collector in

the form of the Withholding Agent who

is made liable for the payment of the tax.

Having withheld the money as tax from payments made to other persons,

the tax collector is made liable by

statute for the payment of the tax so that he is legally obligated to make

payment of the withheld collected funds over to the U.S. Treasury. Again, in the provisions of the statues under

§ 1463, it is the tax collector who is punished for a

failure to pay, not the taxpayer,

and these facts again work to keep the

whole scheme of the income tax legislation, together with all of the

provisions for the collection and enforcement of the income tax, indirect and constitutional.

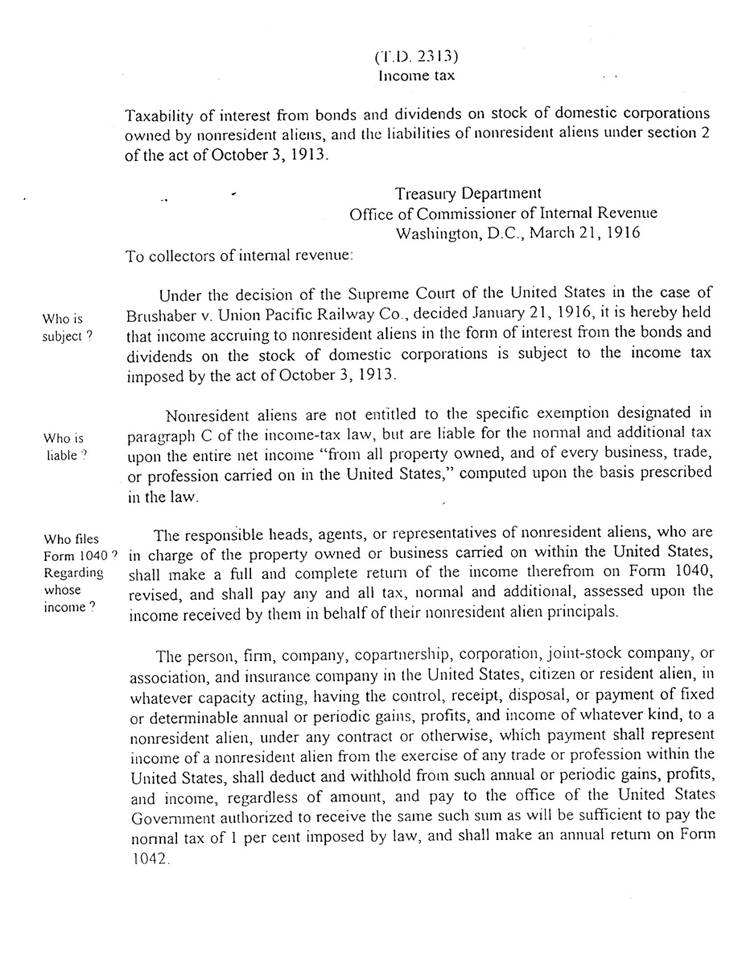

This understanding, that the income tax is actually a foreign tax enacted in the form of a tariff that is collected at the source by withholding tax from the payments made to foreign persons in the United States, is supported by the document issued by the Treasury to the collectors of internal revenue instructing the collectors on how to enforce the law under the newly issued Brushaber decision of the Supreme Court. That document is Treasury Decision 2313 (Exhibit A).

In fact, every single code section that I have been told compels American citizens to pay an income tax on the fruits of their labor in the form of income, when researched, leads to the discovery of more evidence that the income tax is actually a limited tax in the form of a tariff with no requirement in statute for the American citizen to pay on his own income. The results of much of this research is contained within the enclosed small book “The Simple Truth About Income Tax”, which covers the material on Section 61, as well as the true specific requirement that is identified and listed in the statutes to file a return, and specifically which return, and more.

Based on all of these facts and research, I have come to the conclusion, and it is now my contention, that Subtitle A of Title 26 is today nothing more than the income tax provisions of the Underwood-Simmons tariff act of October 3rd, 1913, slightly modified through time, but which still only implements, through the actual written provisions of the statutes, the basic indirect scheme of the income tax identified by the Supreme Court in the Brushaber decision in 1916, of collecting the tax at the source, as the only legitimate application of the tax.

To summarize, it is now easily provable that: Section 1 of Subtitle A does not impose a direct tax on the domestic income of individuals who are American citizens; that Section 61 does not identify domestic “sources” that American citizens are subject to report and pay tax on; and that Sections 6001, 6011 and 6012 do not identify citizens as “persons” required to file a Form 1040 return reporting their own income as taxable. And, that all of this is easily provable today from a simple and uncomplicated reading of the actual provisions of the statutes.

All of this information and much, much more supporting evidence, in the form statutes, regulations, Delegation Orders, Treasury Decisions, Internal Revenue Manual provisions, Supreme Court decisions, etc., are all available from www.tax-freedom.com and are presented in small book “The Simple Truth About Income Tax” by Thomas Freed. I urge you to research the verifiable accuracy of the information presented there.

{If the letter is

to a reporter, include the next paragraph, otherwise remove it}

[Over the past year I have come to enjoy your articles and writing style very much, and consequently, I would like to encourage you to investigate the legal facts that I have presented to you in this letter, and to write a story for publication about the apparent inconsistencies and contradictions that so obviously exist today between the actual written provisions of the income tax statutes and controlling court decisions that I have identified, and the IRS’s de-facto practices and operations regarding the alleged imposition and enforcement of the income tax as a direct tax, which clearly and obviously are not really supported by written law or controlling judicial decisions.]

{If the letter is

to a Judge or other government person, include the next paragraph, otherwise

remove it }

[Consequently, sir, I would like for you to explain to me in a response to this letter how the written Subtitle A income tax laws have been deemed to apply to me or my income, when the statutes so clearly and plainly implement the collection of the income tax through an indirect scheme identified by the Supreme Court in 1916 as a scheme of collecting the tax at the source, that is effected by statutorily defined Withholding Agents, who, acting in the capacity of tax collectors, shift the burden of the tax they pay by collecting tax at the source by withholding it from payments made to subject non-resident foreign persons.

If you could provide a response to help clarify the matters presented in this inquiry it would be greatly appreciated, but sir, I am aware that under the separation of powers established in the Constitution between the three branches of the federal government, the judicial branch and its courts do not make law or change the written law as enacted, so please don’t try and tell me “The courts have determined …”. What I am asking you to do is to provide to me a cite of the specific statute (section number) that makes a person liable for the payment of the income tax on his own income. The only statutes I can identify that establish liability for the payment of income tax are Sections 1461 and 3403, which both clearly establish the indirect liability of the tax collectors to pay over to the U.S. Treasury the income tax that they have collected from other persons by withholding money as tax from payments made to them. Are these the only statutes that actually exist, establishing liability for payment of the income tax, or not? And if not, where are the other Sections located in the Code? Please provide their section numbers to me so that I can look them up and read them! IF no other code section exists, or you yourself are unable to identify one in the statutes for me, please state those facts in your response to me.]

{If the letter is to a

[I would like to encourage this university to consider hosting and participating in a series of public events intended to stimulate intellectual discussion and an expanded knowledge of the information on the law herein presented.]

I look forward to receiving a response from you regarding these matters of critical national importance.

Sincerely,

___________________________

«First

Name» «Last

Name»